Markets appear to have adopted a glass half-full view of the recent election outcome. Oxford Economics cautions, however, that while lower taxes, more infrastructure spending and reduced regulation may be positives for businesses, increased policy uncertainty, more trade protectionism, congressional fiscal orthodoxy and stricter immigration are important constraints.

One of the main characteristics of a Trump presidency will be the unusually elevated degree of policy and political uncertainty. While we know the name of the president and the composition of Congress, we have little information about the likely administration, which policies will be passed and when these may be implemented.

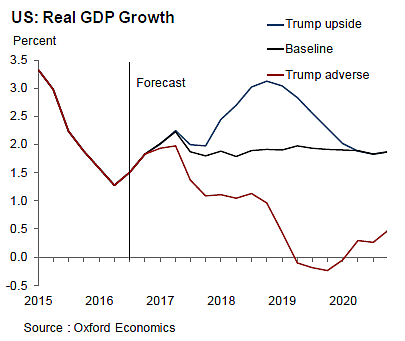

Our baseline view assumes a compromise between President Trump and Congress contains a modestly expansionary fiscal package and targeted trade protectionist measures. While private sector activity benefits from lower taxes and increased infrastructure investment in the near term, trade protectionism and elevated policy uncertainty constrain growth to just 2% in 2017 and 1.8% in 2018. The Fed still raises rates in December, but only proceeds with one rate hike in 2017.

Our upside scenario assumes tax reductions are twice as large as in the baseline (worth $1tn over the next decade) and much more inclusive for low-income families, and the government implements a larger infrastructure investment program. Trump negotiates a relaxation of fiscal orthodoxy in exchange for a less protectionist trade stance than he campaigned on. Growth accelerates to 3% in 2018, and the economy is 2% larger than in the baseline by the end of 2020, creating 2 million more jobs.

Our downside scenario assumes that, after a brief honeymoon period, President Trump reverts to his highly protectionist and isolationist stance. His refusal to negotiate with Congress means Republicans refuse any increase in the deficit. Global aversion to the US combines with heightened domestic policy uncertainty. Real GDP growth slows and the economy enters a recession by late 2018. By the end of his term, the economy is 5% smaller than in the baseline and counts 4 million fewer jobs.

Oxford Economics is one of the world’s independent global advisory firms, providing reports, forecasts and analytical tools on 200 countries, 100 industrial sectors and over 3,000 cities.